Intervention Study

How the Study Was Conducted

Our intervention study was a 5-day diary study exploring how AI-assisted reflection affects awareness and behavior around unplanned spending. We recruited 7 participants across different life contexts, including a professional organizer, a Ford Foundation fellow, a community residence supervisor, UCLA and community college students, a part-time tutor, and two nursing program students. The diverse spread of participants was intentional as we wanted to see how spending psychology and receptivity to reflection varied across income levels, daily routines, and financial pressures.

Each participant interacted with a ChatGPT agent twice daily. In the morning, they logged their planned purchases for the day. In the evening, they reported any unplanned purchases and engaged in a reflective dialogue with the AI, which asked follow-up questions about the context, motivation, and feeling behind each purchase. We also conducted pre- and post-study interviews to capture baseline spending psychology and assess what changed.

Our key question for our study was as follows: Does enforcing intentional purchase planning create awareness of impulse/unplanned spending patterns, and if so, will that affect the impulse spending behavior? What emotional and social patterns drive unplanned purchases in the first place (aka what is an impulse?)?

Five Key Insights

- Awareness increased, but behavior change exists on a timeline much larger than that of our study. Almost every participant reported feeling more conscious of their spending, but most continued making similar purchases. Lyn put it directly: “It made me more aware of my spending. Didn’t change the spending, but made me more aware of it instead of not being aware of it.” Five days was enough to bring awareness to the behavior, but it was not enough to shift habits.

- Unplanned purchases have an emotional infrastructure that dictates which item specifically is bought. Purchases clustered into predictable emotional logics: mood regulation (buying food in response to a bad day), social compliance (buying to match what your group is doing), FOMO mindset (framing a purchase as a once-in-a-lifetime opportunity), and reward logic (treating yourself as deserved). The AI was most valuable when it surfaced these patterns to participants who hadn’t consciously named them before. Courtney, for example, realized mid-week that she spends freely on others but feels intense guilt spending on herself, and she let us know that she acted on that insight after the study ended!

- Social context was the biggest unplanned purchase trigger, yet it produced the least guilt. Participants bought things they hadn’t planned almost exclusively in social settings, and almost all felt fine about it afterward. Andres joined his nursing cohort at a coffee shop on day one of clinicals. Audrey went out to eat with friends even when she had food at home. Courtney spent $15 at McDonald’s on a declared no-spend day to cheer up her sister and felt no regret. This tells us that any financial reflection tool needs to account for the relational meaning of spending, not just treat it as an individual decision.

- Planning the day’s purchases was often more impactful than the evening reflection. The morning ritual created a kind of pre-commitment that changed in-the-moment decision-making. Erick stopped himself from buying a $2 item at a discount store, Courtney talked herself out of boba tea, and Lyn’s bed pillows kept getting deprioritized as she planned each day until she realized they just weren’t that important to her. The planning introduced a natural friction point that illuminated each unplanned purchase in real time.

- People quickly grew tired of AI coaching’s persistence. Participants appreciated the non-judgmental, consistent tone, especially for logging purchases they might feel embarrassed about. What didn’t work was the volume of follow-up questions. Erick: “All right, chill out.” Taylor felt it “probed and probed and probed.” Lyn compared the experience to being stalked. The AI’s neutrality also degraded over longer sessions, drifting toward gentle validation, which Courtney called “a little manipulative, even if it was trying to be kind.” We learned that responsive calibration matters enormously: fewer questions for small purchases, tighter guardrails on reframing, and proportional depth based on the size and emotional weight of what’s being discussed.

Our Solution Design – Changes

From our study, we saw three distinct personas.

- Engaged Reflectors (Courtney, Taylor, Lyn) genuinely used the AI conversations to generate psychological insight and were the most likely to feel both the value and the discomfort of the tool.

- Tracker Preferrers (Audrey, Erick, Briant) valued the logging and planning but found the emotional inquiry excessive; Audrey said she’d prefer a version without the AI entirely.

- Social Rationalizers (Andres, Pierre) used the reflections to verbalize their existing reasoning rather than interrogate it, and their spending was so socially embedded that individual reflection had limited traction.

This typology has many implications for how our solution should be designed; along with the key insights we gathered, we understand that our platform has to, in some way, account for the high frequency of impulse spending that occurs in social spaces. Even when users are thoughtful and reflective about their behaviors when they’re alone, it seems as though there is trouble recognizing impulse spending in the moment when they’re with others. Additionally, the study provided helpful guides on how we should design our AI; its tone needs to adapt to what a user needs and has to be able to recognize what those needs might be.

System Path

Our interconnected system path demonstrates the points of connection between each of our personas. Though the key goal throughout our platform is to help users overcome impulse spenders, we created this map as an exercise to better understand how we could make a holistic experience within the platform for a variety of different backgrounds.

Story Maps

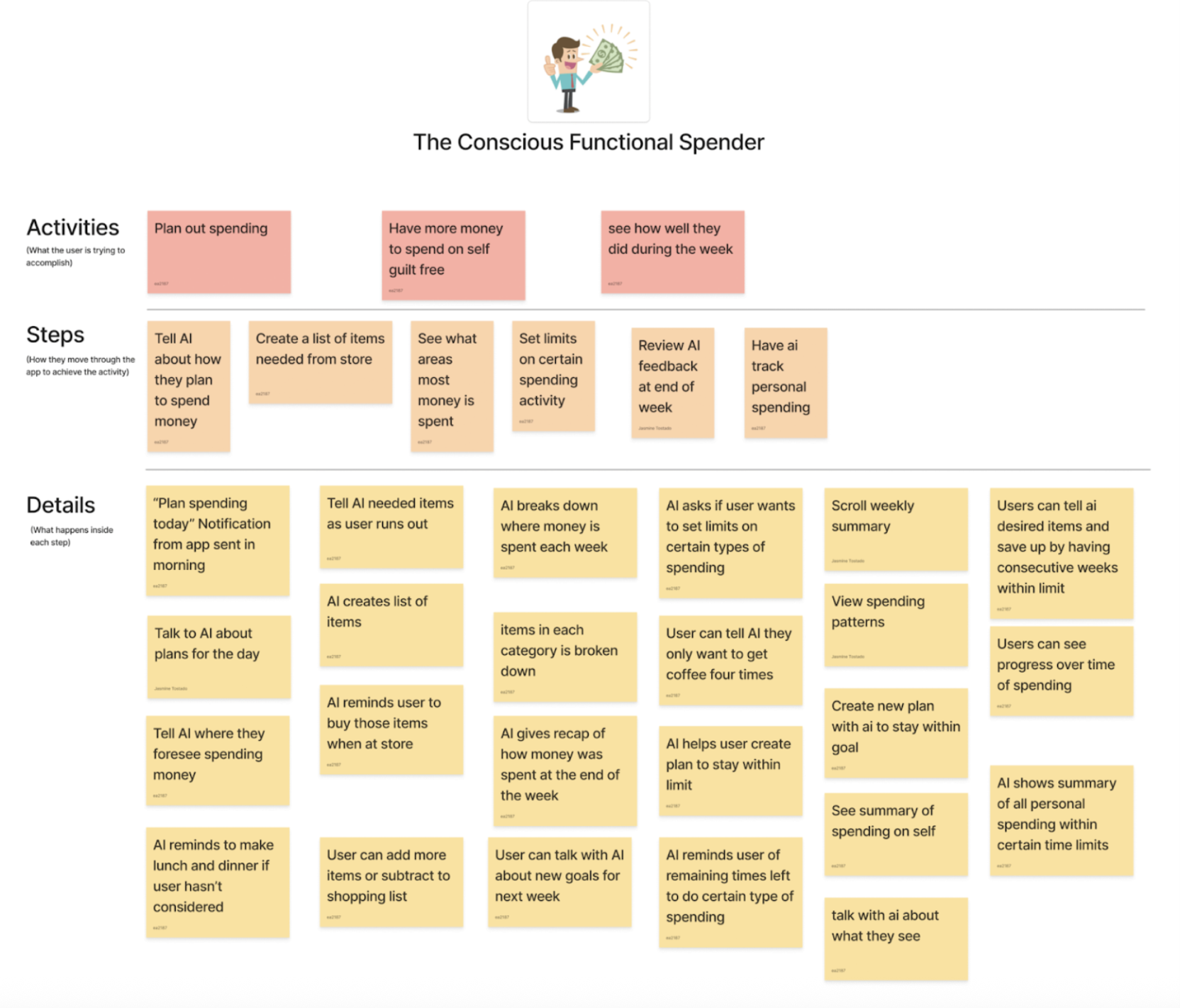

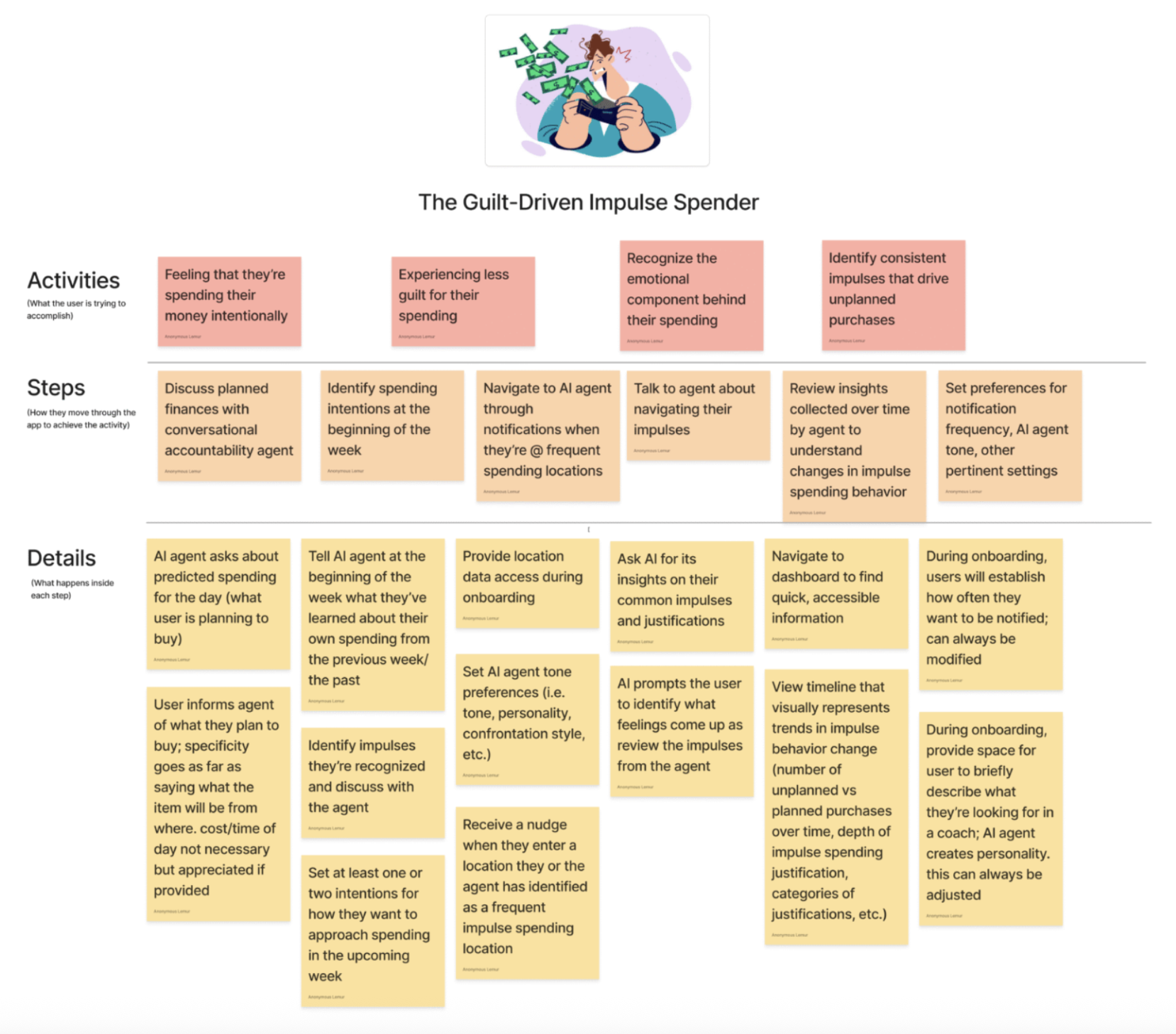

When getting into the mindset of the Guilt-Driven Impulse Spender persona, I thought about what this person might want to accomplish when they decide to use this platform. In their case, they seek to not only understand what it is that causes them to spend impulsively, they mostly want to stop feeling so intensely guilty about it. This was a tricky revelation to design around because the goal of our platform is not to blindly support purchases in the interest of keeping users happy; we want to coach people through their behavior change, making them feel supported while also delivering the pushback, clarity, and bluntness that they’re not currently giving themselves. Some of the MVPs that came as a result of this insight and this story map include:

- Coach personalization: Users can provide a description of desired coaching personality during onboarding so that they can receive guidance in the manner that best suits them.

- Below-the-surface prompting specification: Prompting the coach to share identified impulses and help the user uncover the emotions behind them

- Visual progress tracker: Utilize this persona’s tendency towards guilt in a way that encourages them to stick to their own goals while still avoiding discouragement or excessive self-punishment when they don’t.

MVP Features

Below we describe our MVP features and how our story maps lead to these features:

Feature 1: AI Chat

Our application will include an AI Chat where users reflect on spending and set financial goals. This feature emerges from all four story maps, where our personas engage in conversational and reflective behaviors. The Conscious Functional Spender story map highlights that this feature might be used for discussing spending plans. The Social Spender story map highlights that this feature could be used to help curate social activities that fall within budget or to engage in reflective discussions about social spending. The Guilt-Driven Spender story map highlights that this feature can be used to derive insights on common impulses and to ask about predicted spending.

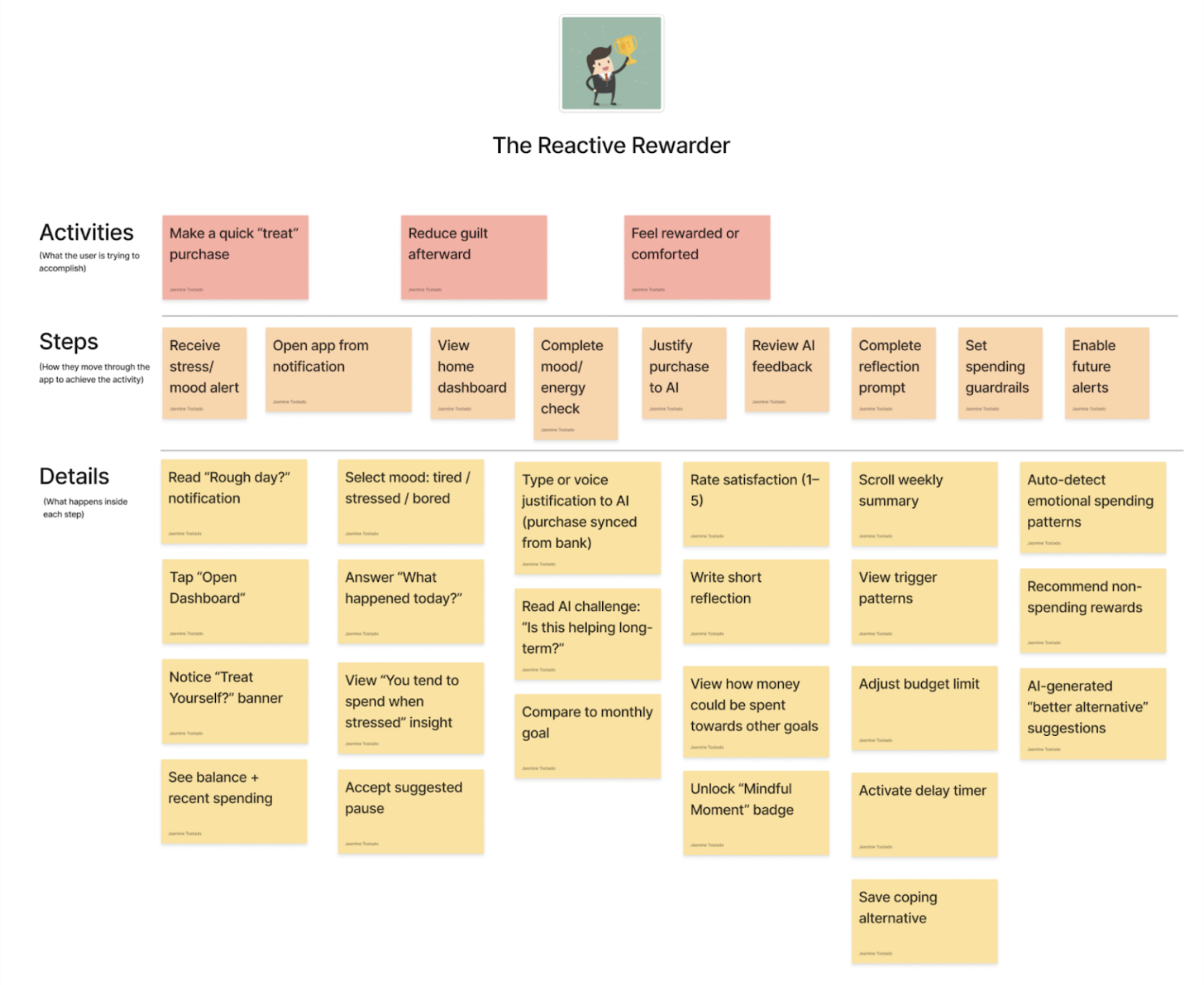

Feature 2: Context-aware push notifications and reminders

By incorporating context-aware push notifications and reminders, we hope to help disrupt impulsive spending patterns as they happen. For example, we plan to send notifications to users when they are in high spend areas. This connects to the Reactive Rewarder story map, where while this persona attempts to make a quick “treat” purchase, we will send them a notification that checks in on their mood and helps them reflect on a plan or set guardrails for the future.

Feature 3: Mood Check-In

Our application will include a mood check-in that captures how the user is feeling when they are at a spending hot spot. Our story map highlighted personas who impulse spend based on emotions and feelings (e.g., Reactive Rewarder, Social Spender, and Guilt Driven Impulse Spender). Hence, this feature serves to (1) help check-in on how users are feeling when they are about to impulse spend and (2) allow our application to use this information to help remind users of their impulsive spending goals.

Feature 4: Daily Spending

Our application will include a feature that allows users to describe what they plan to spend money on a given day. For Reactive Rewarders, whose story map indicates they are motivated to make a quick “treat” purchase, daily intention setting functions as a guardrail and can help provide insights into trigger patterns for unplanned spending. This feature also emerges from story map steps such as “identify spending intentions at the beginning of the week” (Guilt-Driven Impulse Spender) and “tell AI about how they plan to spend money” (Conscious Functional Spender).

Feature 5: Weekly Spending Goal Progress

Our application will include weekly spending goal progress where users can see how well they stuck to their spending plan. This connects to the Conscious Functional Spender story map, representing a persona who aims to see how well they did with their financial goals by using our app to view spending patterns and see progress over time. Furthermore, the Reactive Rewarder Spender scrolls weekly summaries and the Guilt-Driven Impulse spender reviews insights collected over time.

Feature 6: Impulse Spending Breakdown

Our dashboard will include a feature that allows users to see a breakdown of their impulsive spending. A detailed breakdown will showcase how much a user spent in each category and the amount of money spent impulsively within different time frames specified by the user. Our Conscious Functional Spender storymap highlighted users who prefer to plan out their spending. Hence, they could use our application to track their spending and scroll through their weekly detailed summary.

Feature 7: AI Personality Customization

Our application will allow users to customize the personality of their AI conversational agent. This connects to the storymap of the Guilt-Driven Impulse Spender, who wants to experience less guilt for their impulse spending. They could modify the personality of this AI that would be most conducive to helping support this goal.

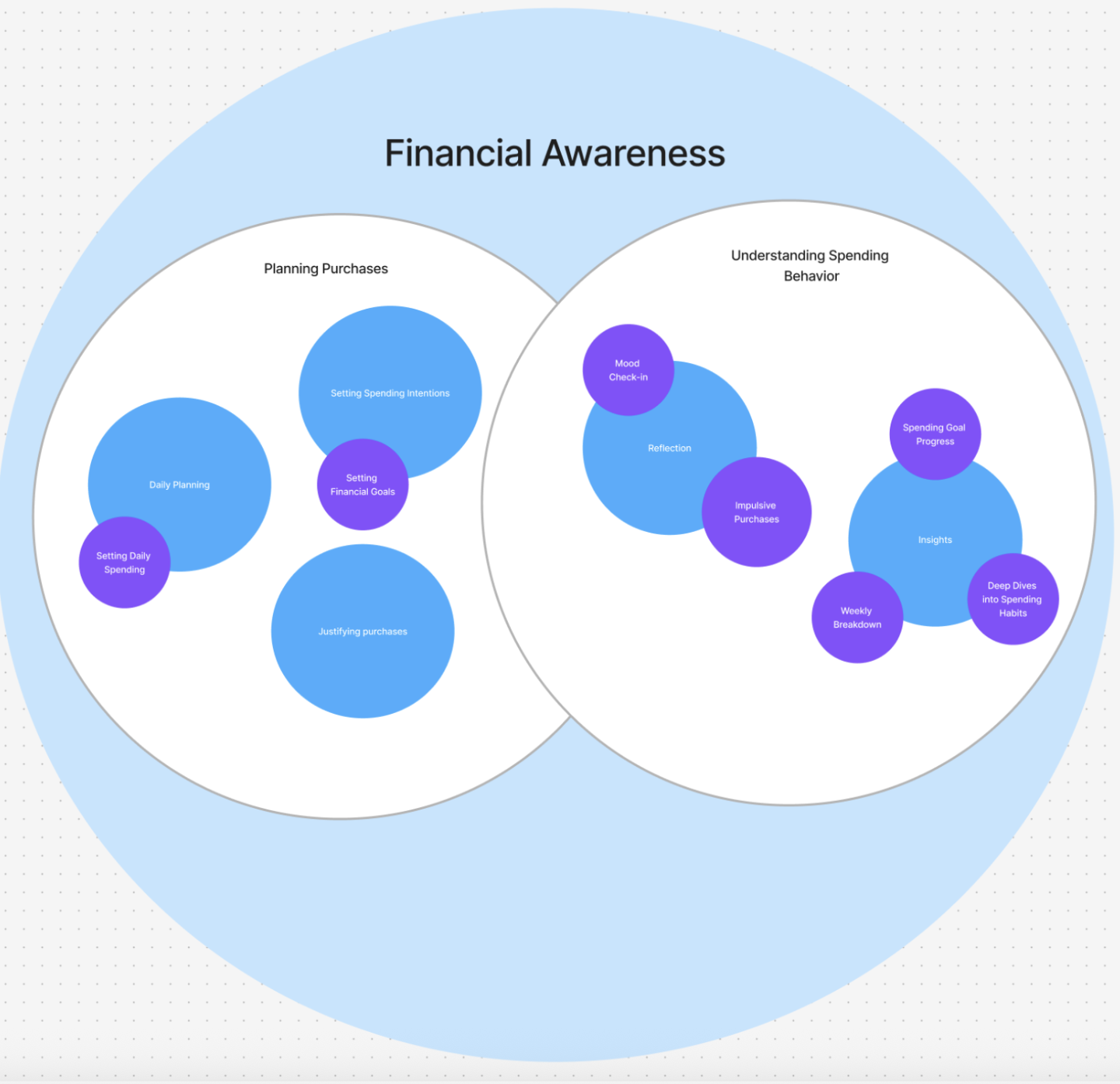

Bubble Map

Process and Key Insights

In this step, I mapped out the different components that contribute to financial awareness. I divided them into two main categories: Planning Purchases and Understanding Spending Behavior. This helped me organize the space and think more clearly about where different features or interventions would fit.

On the planning side, I included daily planning, setting spending intentions, setting financial goals, setting daily spending limits, and justifying purchases. These actions focus on decisions made before or during spending. I realized that even when people plan, they still justify purchases in the moment, which makes planning alone insufficient.

On the understanding side, I included mood check-ins, reflection, identifying impulsive purchases, weekly breakdowns, tracking spending goal progress, insights, and deeper dives into spending habits. These activities focus on analyzing behavior after spending has already occurred. They are less about control in the moment and more about awareness over time.

One key insight is that financial awareness is not only about tracking expenses. It also includes emotional and behavioral elements, such as mood and impulse recognition. This suggests that a traditional budgeting approach would not fully address the problem. The solution needs to support behavioral reflection, not just financial tracking.

Another insight is that planning and reflection are related but separate skills. A person may set clear goals but still struggle with impulsive purchases. Someone else may understand their patterns but fail to change them. This shows that awareness and behavior change do not automatically happen together.

Overall, this step helped me see that improving financial awareness requires both proactive planning and reflective understanding. The most meaningful opportunity appears to be connecting these two areas in a way that helps users translate awareness into better decisions over time.

Assumption Tests

Assumption #1: Impulse Spenders Want To Stop.

- Why this matters: Because our platform is centered around helping impulse spenders stop impulse spending, it is critical that they actually have a desire to do so; this matters in terms of both discovery and retention since we need the desire to stop to drive users onto the platform and keep them there. Without this assumption being true, the crux of our current approach to financial betterment will need to be redefined.

- Methodology: I plan to ask in as many spaces as I can whether or not, depending on if you consider yourself to be an impulse spender, you want to stop impulse spending. I’ll provide the options of “Yes, Kind of, Not really, & Not at all” to see if providing a range of feelings shows more than a binary response that might fail to capture nuance. If there is time, I’ll follow up with some people who responded with each answer to better understand their reasoning for their selection, and from there, these insights will better inform the validity of the assumption. As far as medium goes, I plan to use the polling features on Instagram, GroupMe, and WhatsApp within the different community spaces I’m a part of.

- Timeframe: Due to the tight turnaround time and the length of polls on Instagram/GroupMe/WhatsApp, I’ll collect responses over 24 hour periods.

- Hypothesis: Because our platform’s current frame relies on this assumption so heavily, I predict that the testing will confirm that assumption is correct.

Assumption #2: People won’t get too frustrated using AI

- Why this matters: Interacting with a conversation AI agent to reflect on spending is a core aspect of our application. If users experience high levels of frustration during this interaction, then they may choose to opt-out of this core part of the intervention.

- Method: We will conduct a quick poll on how frustrated people feel when using AI conversation agents for reflection-based use cases:

- Questions:

- On average, how frustrated do you feel when using AI tools to reflect on your thoughts or experiences?

- 1 – Not frustrated at all

- 2 – Slightly frustrated

- 3 -Moderately frustrated

- 4 – Very frustrated

- 5 – Extremely frustrated

- What types of reflection have you used AI for?

- Timeframe: We will collect responses over the course of 24-48 hours.

- Hypothesis: There will be an average frustration score less than or equal to 3.

Assumption #3: People recognize which purchases are impulse purchases.

- Why this matters: To validate the hypothesis that people can accurately recognize impulse purchases. This matters for our application because without it, our application will not be able to reliably track impulse spending and support meaningful reflection on impulse purchases.

- Method: Present participants with three short purchase scenarios, two that qualify as impulse purchases by definition and one that has been clearly planned. Then ask participants to classify each scenario as either “Impulse” or “Not Impulse.

- Scenarios

- Kathy has been thinking about buying an iPad for two months and went yesterday to go buy it

- Mario was passing by Starbucks, realized he felt tired, and bought a coffee.

- John was at the store and bought three bags of chips since he saw they were on sale

- Hypothesis: At least 70% of participants correctly classify the scenarios according to the predefined impulse criteria.

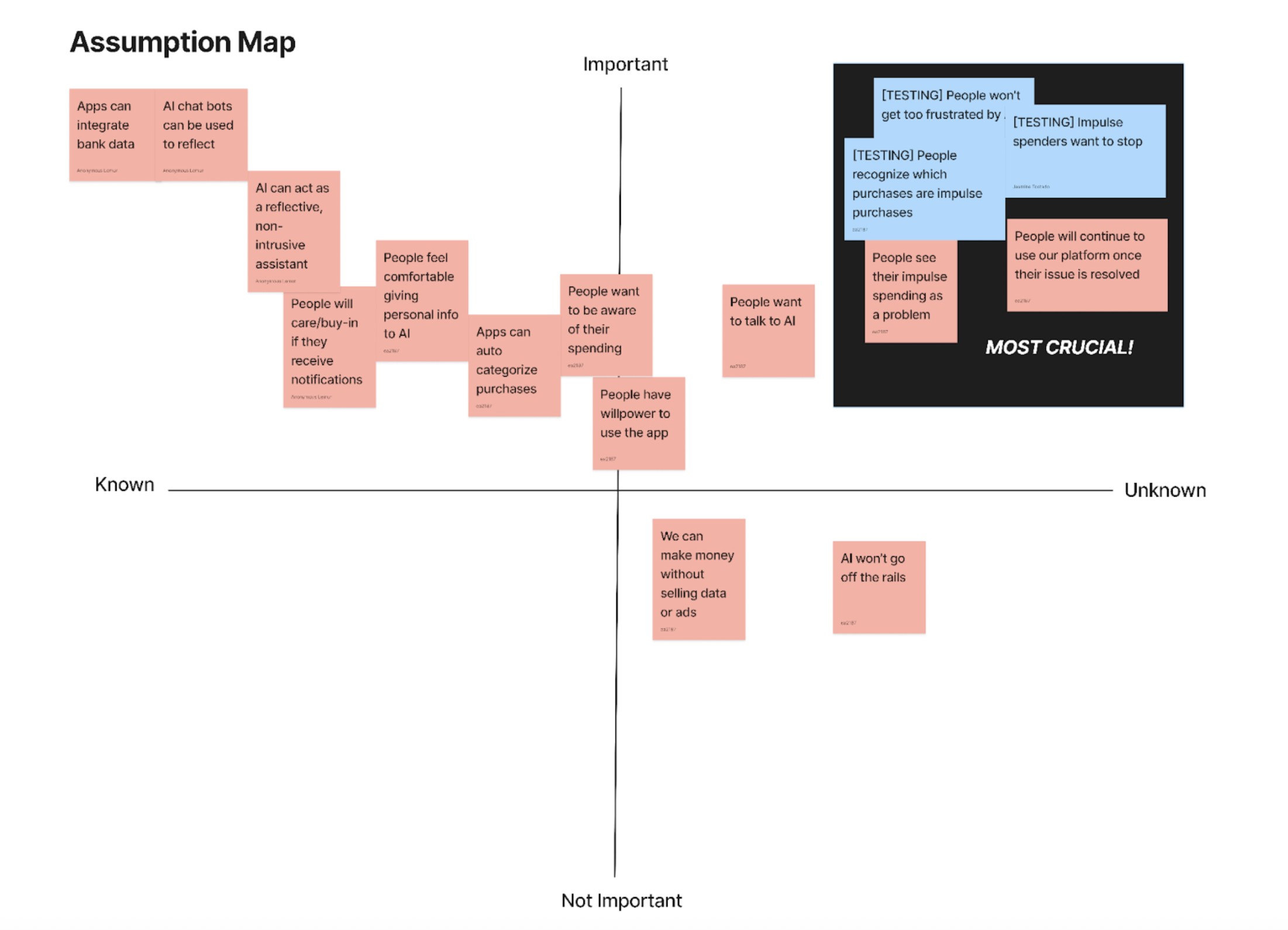

Assumption Map

Key Insights from Creating Our Assumption Map

After mapping our assumptions, we realized that the biggest risks in our idea are psychological.

Most of the assumptions in the “most crucial” quadrant relate to whether people actually see their impulse spending as a problem and whether they genuinely want to stop. If users don’t feel internal tension about their spending habits, then the product won’t matter, no matter how well the AI works. This suggests that motivation is the core dependency of the entire idea.

Another key insight is that recognition comes before intervention. If people cannot correctly identify which purchases are impulse purchases, then reflection with AI will not be effective. The product relies on users agreeing, at least somewhat, with the framing of their behavior. If the AI labels something as impulsive and the user disagrees, trust could break down quickly.

We also noticed that frustration is a major retention risk. Even if people want to change, they will stop using the platform if interacting with the AI feels annoying, repetitive, or judgmental. So emotional experience may matter just as much as functional accuracy.

Finally, this map clarified that we are building for a specific type of user: someone who already feels uneasy about their impulse spending and wants to improve. The product likely will not work for users who do not perceive their behavior as problematic.

Overall, the assumption map helped us see that the success of this idea depends more on user psychology and readiness for change than on technical capability.