Baseline Study

Study Purpose

The purpose of this study is to investigate impulse and habitual daily spending habits. We are especially interested in convenience purchases (e.g., coffee, snacks, food delivery, rideshare, etc.) that add up over time. Through a longitudinal diary study tracking spending habits and reflections, we aim to address the following research questions:

- What types of convenience-based purchases occur most frequently in participants’ daily lives?

- What situational contexts (e.g., time of day, location, social setting, emotional state) are associated with impulse or habitual spending decisions?

- For those who’d like to reduce their spending, what are the common factors and motivations associated with convenient purchases?

- How aware are impulse spenders of their impulsive purchases (as defined by an unplanned purchase made for no particular reason, according to the spender)?

Study Methodology

We conducted a diary study that combined qualitative and quantitative data collection through surveys and structured interviews. The study began with broad recruitment through an online screener designed to collect demographic information and baseline spending habits. Based on screener responses, we selected nine participants who met our eligibility criteria.

Selected participants first completed a 30-minute pre-study interview, during which we gathered contextual information about their spending behaviors and introduced the study protocol. Participants also received an instruction document outlining the study’s purpose, expectations, and participation guidelines.

Over five consecutive days, participants logged their daily spending and reflections using Google Forms. After each purchase, participants completed a short diary entry describing the transaction and their emotional response. To reduce participant burden and minimize drop-off, the form included a limited number of focused questions. Participants were allowed to submit multiple entries at once if they forgot to log a purchase in real time. We also sent daily reminder messages to encourage consistent participation.

At the end of the diary period, participants completed a 30-minute post-study interview to reflect on their experiences and provide additional context for their recorded behaviors.

This approach allowed us to collect both quantitative data (e.g., spending frequency, cost ranges, impulsivity and guilt ratings) and qualitative data (e.g., motivations, emotional responses, environmental context), enabling a comprehensive analysis of impulse spending behavior.

Data Collection

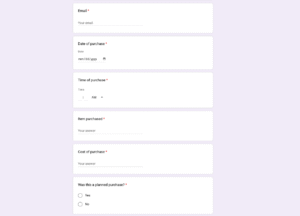

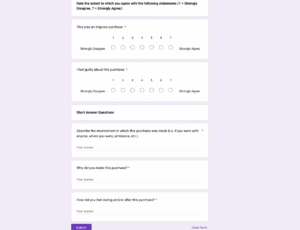

Participants recorded purchases using a Google Form that could be submitted multiple times throughout the day. This flexible format allowed participants to log purchases when convenient and to retroactively record missed entries.

Each diary entry included the following components:

Logistical Data (Quantitative)

- Date and time of purchase

- Item purchased

- Cost (in predefined ranges)

- Whether the purchase was planned (Yes/No)

- Agreement ratings (1–7 scale) for:

- “This was an impulse purchase”

- “I felt guilty about this purchase”

Content Data (Qualitative)

- Description of the purchasing environment (location, social context, ambience)

- Reason for making the purchase

- Emotional response during and after the purchase

This structure enabled systematic comparison across participants while preserving rich contextual detail.

Participant Recruitment

We recruited nine participants who regularly engaged in convenience spending, including frequent purchases of coffee, fast food, food delivery, prepared meals, and in-app purchases. This population was selected because of their predisposition toward recurring discretionary spending.

Participants were recruited through word of mouth, flyers, and community platforms such as Nextdoor. Interested individuals completed an online screener to assess eligibility based on their spending frequency and habits. Only participants who demonstrated consistent convenience spending were selected for the study.

The final sample represented a group of users with recurring exposure to impulsive and situational purchasing decisions, making them well-suited for examining patterns of impulse spending and justification.

Grounded Theory

Through our diary study, interviews, and qualitative analysis, we developed several grounded theories that explain how participants experience and make sense of impulse spending. Our findings show that impulse purchases are rarely driven by a lack of financial knowledge. Instead, they are shaped by situational pressures, personal values, and real-time justification. Participants actively constructed explanations for their spending that allowed them to feel responsible rather than impulsive.

A central pattern across our data was rapid reframing. Participants often made unplanned purchases in response to hunger, fatigue, time pressure, or convenience, then quickly labeled these decisions as necessary, productive, or goal-aligned. Food was framed as fuel, beauty products as maintenance, and organizational items as investments. This reframing reduced guilt and limited motivation to change behavior, even when users recognized that the purchase was avoidable.

We also found that many participants underestimated the true scope of their everyday spending. Small, routine purchases such as coffee and snacks became “invisible” within broader financial perceptions. Most participants relied on rough mental estimates rather than concrete tracking. Logging disrupted this pattern by making spending more visible. For some users, this led to greater mindfulness, while for others it reinforced existing habits by validating their self-image as reasonable spenders.

Spending decisions were also closely tied to identity and social context. Participants judged purchases based on whether they aligned with their values and roles, such as being responsible, productive, or supportive of others. Purchases for family, health, or social connection were consistently viewed as acceptable, even when costly. In contrast, spending for personal enjoyment alone often triggered greater internal conflict. Retail environments further amplified this behavior by encouraging “while I’m here” logic, leading to scope expansion that felt efficient rather than impulsive.

Together, these grounded theories show that impulse spending is driven by context, justification, and identity rather than simple lack of control. Participants normalized impulsive behavior through environmental cues, personal narratives, and value alignment. Our full grounded theory report expands on these patterns in detail. This framework guided our intervention design by emphasizing the importance of targeting high-risk moments, increasing meaningful visibility, and interrupting real-time rationalization.

System Models

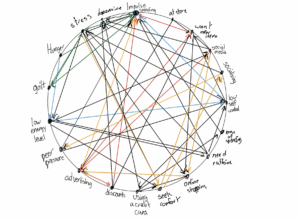

Connection Circle

This connection circle represents impulse spending as a network of interacting emotional states, social contexts, and structural conditions that influence behavior over time. Emotional factors such as stress, hunger, guilt, low energy, and low self-control increase susceptibility to impulsive purchases, while situational contexts like being in a store, socializing, and exposure to social media or advertising introduce desire and opportunity. Financial features including discounts, ease of spending, online shopping, and credit card use lower the effort required to complete a purchase, making spending feel accessible and reasonable in the moment. Impulse spending produces short-term dopamine and emotional relief, which temporarily reduces stress, but often leads to guilt afterward. This guilt contributes to increased stress, creating a feedback loop in which stress and guilt reinforce one another and further heighten vulnerability to future impulse spending.

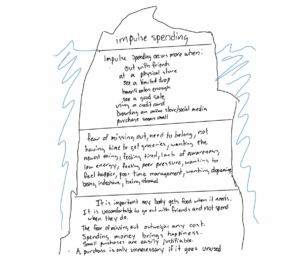

Iceberg Model

This iceberg model represents impulse spending by separating visible behaviors from the deeper, less visible factors that drive them. On the surface, impulse spending appears in specific situations, such as being out with friends, shopping in physical stores, seeing limited-time drops or good sales, browsing online stores or social media, using a credit card, or making purchases that seem small and insignificant. These moments are easy to observe and often feel harmless, which makes the behavior socially acceptable and difficult to challenge in the moment. Beneath the surface are emotional and psychological drivers, including fear of missing out, a need to belong, peer pressure, fatigue, stress, low energy, poor time management, and a desire for dopamine or short-term happiness. These factors reduce self-control and increase the appeal of immediate rewards, especially when awareness is low or decision-making feels overwhelming. At the deepest level are core beliefs that justify and sustain the behavior over time. These include the belief that spending money brings happiness, that small purchases are easily justifiable, that it is uncomfortable or unacceptable to abstain when friends are spending, and that fear of missing out outweighs financial cost. There is also the belief that a purchase is only unnecessary if it goes unused, which reframes most spending as reasonable after the fact. Together, these layers show that impulse spending is not just about poor financial discipline, but about emotional regulation, social belonging, and deeply held assumptions about comfort, happiness, and necessity.

Secondary Research

Our previous blog post synthesized eight articles on impulse and habitual spending. Main insights drawn from these articles are as follows:

- Impulse spending is triggered by environmental and emotional cues. Our articles identified that being in proximity to a product or receiving alerts for discounts can cause someone to make unplanned purchases. Moreover, feelings of FOMO, boredom, and negative mood, in addition to a desire to fulfill psychological, social, and emotional needs, were drivers for this behavior as well.

- Spending ecosystems are designed to trigger impulsive behavior. While users exercise some control over their spending behavior, our articles revealed that retailers design platforms to encourage spending and minimize friction. Incorporating social influence, rewards/discounts, and refund policies are intentional choices that reduce perceived spending risk.

- Intervention can entail disrupting cues, reflection, and proactivity. Our articles also addressed a number of intervention approaches to curtailing impulsive spending behavior. This included proactively strategizing, encouraging reflection, imposing spending limits, and enforcing delays before purchase.

- Personalization is important for effective intervention. One article highlighted that identifying a user’s emotional needs is critical for creating reflective interventions that address the root cause. Another indicated that spending reduced more when users reviewed their own financial self-control strategies compared to strategies from others.

Behavioral Persona Synthesis

Based on cross-analysis of our individual behavioral personas, diary studies, interviews, and affinity mapping exercises, we synthesized our findings into three core behavioral personas that represent the most salient and recurring impulse spending patterns within our participant pool. These personas were selected because they consistently appeared across multiple participants and data sources, captured distinct motivational and emotional drivers, and revealed meaningful intervention opportunities.

Rather than segmenting users by demographics, these personas reflect shared behavioral dynamics that shape how and why impulse spending occurs. Together, they cover a broad spectrum of our target audience and highlight different breakdown points in self-regulation, financial intention, and emotional decision-making.

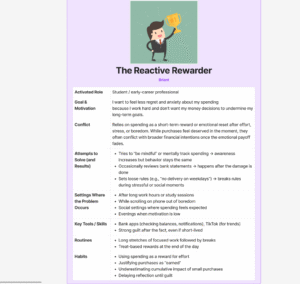

1. The Reactive Rewarder

Overview

The Reactive Rewarder uses spending (especially on food and small treats) as a reward after effort, stress, or physical depletion. This persona emerged most strongly from Briant’s data and was reinforced by patterns across multiple participants.

Why This Persona Matters

This persona is characterized by a persistent gap between intention and execution. Users express a desire to improve their financial habits, recognize patterns of overspending, and reflect on their behavior, yet consistently fail to change because spending occurs in moments of fatigue, hunger, or low cognitive bandwidth.

Their purchases are framed as “earned,” “necessary,” or “deserved,” which minimizes guilt and delays reflection until after the transaction. As a result, traditional budgeting tools insights are ineffective for this group.

Key Insight

Impulse spending for this persona is driven more by timing and energy than by lack of financial knowledge. Interventions must occur before or during depleted states, not after.

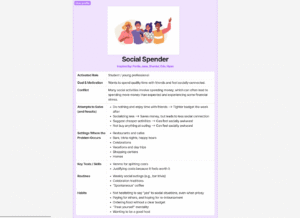

2. The Social Spender

Overview

The Social Spender’s purchasing behavior is shaped primarily by social context. Spending increases when users are with friends, family, coworkers, or partners, and is often justified as part of maintaining relationships.

Why This Persona Matters

Across interviews and diary entries, social environments consistently emerged as high-risk contexts for overspending. Participants described feeling pressure to conform to group norms, discomfort around suggesting cheaper alternatives, and difficulty maintaining personal budgets in collective settings.

Although these purchases are typically viewed as “worth it,” they frequently become moments of delayed financial stress, especially when users later review their spending.

Key Insight

For this persona, financial decisions are social decisions. Spending is less about individual preference and more about belonging, reciprocity, and avoiding social friction.

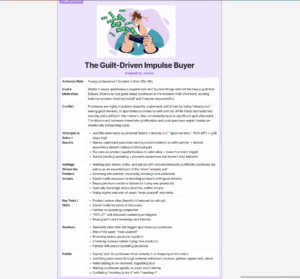

3. The Guilt-Driven Impulse Buyer

Overview

The Guilt-Driven Impulse Buyer makes frequent unplanned purchases driven by spontaneity, convenience, and exposure to external stimuli (reviews, discounts, partner influence, and trending products).

Why This Persona Matters

This persona experiences the strongest emotional volatility around spending. Purchases feel exciting and justified in the moment, but are followed by intense guilt and regret. Unlike the Reactive Rewarder, this group does not successfully neutralize guilt through rationalization.

They attempt to manage regret through research, external validation, and deal-seeking, but these strategies fail to prevent repeated impulsive behavior. Avoidance of tracking further reinforces the cycle.

Key Insight

This persona is trapped in a loop of excitement, justification, regret, and avoidance. Emotional regulation, not information access, is the primary challenge.

Rationale for Persona Selection

We selected these three personas because they:

- Appeared consistently across participants and data sources

- Represented distinct psychological and situational drivers of impulse spending

- Revealed different breakdown points in self-control and reflection

- Offered complementary perspectives for intervention design

- The Reactive Rewarder highlights vulnerability during depleted states.

- The Social Spender reveals how social norms override personal budgets.

- The Guilt-Driven Impulse Buyer exposes the emotional costs of impulsivity.

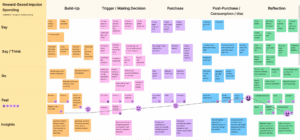

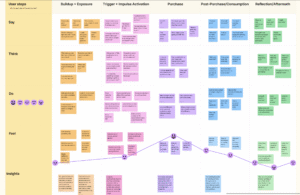

Journey Map Synthesis

Each persona is supported by a corresponding journey map that visualizes how impulse spending unfolds over time. While individual experiences vary, strong structural similarities emerged across participants.

Key Cross-Persona Insights from Journey Maps

- Context matters more than intention: Users’ environments (social settings, physical locations, time of day, and emotional states) had greater influence than stated financial goals.

- Justification happens in real time: Participants actively constructed narratives (“I needed this,” “It’s worth it,” “I earned it”) to enable purchases in the moment.

- Emotional outcomes diverge by persona:

- Reactive Rewarders neutralized guilt quickly

- Social Spenders prioritized connection over cost

- Guilt-Driven Buyers experienced lingering regret

Strategic Value for Design

Synthesizing these personas and journeys allows us to design interventions that are:

- Context-aware (targeting high-risk moments)

- Emotionally responsive (addressing guilt and reward)

- Socially sensitive (supporting group decision-making)

- Proactive rather than reactive

By grounding our design direction in these three personas and their associated journeys, we ensure that future solutions address the real behavioral mechanisms underlying impulse spending rather than relying solely on informational or budgeting-based approaches.