Introduction

We are Team Aardvark, and our mission this quarter is to design a tool that helps curb impulsive and habitual daily spending for individuals seeking to save more money. To inform our design process, we conducted a literature review and comparative analysis to examine existing solutions, identify effective strategies, and uncover gaps in the current landscape.

Overview: Analysis of Existing Comparators

The comparators we chose to analyze represent the desire to help users budget/save money as well as solve a variety of other problems and solutions related to healthy spending: PocketGuard, Cleo, Everydollar, Upside, Mint, Rakuten, Honeydue, and Penny Finance. Let’s take a closer look at these comparators.

Comparator Deep Dive

Jasmine

Pocket Guard

Website

Description

PocketGuard is a personal finance app designed to show users how much money they have “in their pocket” after accounting for bills, saving goals, and necessities. It positions itself as an all-in-one money management platform, offering automated budgeting through direct connectivity with financial institutions to pull transaction data. Key features include spending insights, recurring payments, goal setting, personalized financial plans, and bill-lowering services (e.g. negotiating cell phone and cable bills). PocketGuard also supports investment tracking, real estate, and net worth calculation, suggesting a target audience of users who want high visibility into their entire financial ecosystem. Overall, the app is geared toward individuals who want to take control of their finances through automation and customization, particularly those managing multiple financial assets and long-term goals.

Strengths and Weaknesses

A major strength of PocketGuard is its breadth of features and seamless integration with external financial accounts, allowing users to view all transactions and accounts in one place. The automation reduces manual effort and provides a comprehensive snapshot of financial health. However, a key weakness is that the app appears better suited for users who already have financial literacy and discipline. While it shows how much discretionary money remains, it does not actively support users who struggle with impulsive or emotional spending. The spending insights feel technical and predictive, relying on AI-driven calculations rather than behavior-focused nudges, reflection prompts, or guidance on how to improve spending habits within specific categories. This created a gap for users who need more intentional support to change their spending behavior, rather than simply monitor it.

Cleo

Website

Description

Cleo is centered around an AI chatbot/financial assistant that provides budgeting advice using humor, sarcasm, and tough love. The chatbot roasts users for poor spending decisions while offering insights into income, expenses, and remaining discretionary spending. Cleo incorporates behavioral challenges, such as setting weekly spending caps for categories like coffee, and light gamification features (e.g., “take a wild guess on how much you spent this week”). A notable feature is its integrated high yield savings account, which includes multiple modes, such as a “swear jar” that automatically fines users for spending at guilty pleasure stores and redirects that money into savings. The app targets users who recognize they have serious spending issues and are receptive to blunt feedback, guilt-based motivation, and punitive mechanisms to curb impulsive behavior.

Strengths and Weaknesses

Cleo’s primary strength is its distinctive personality-driven approach, which can be effective for users who respond to accountability through guilt and small punishments. Features like automated budgeting, transaction syncing, high-yield savings, and credit-building tools add tangible financial value beyond the chatbot experience. However this guilt and punishment-heavy model can be counterproductive for many users, as shame often reinforces impulsive spending rather than encouraging long-term behavior change. The app emphasizes restriction and fines without reflection or learning, which may limit sustained improvement. A key gap we aim to fulfill is the lack of positive reinforcement, such as a reward-based model that celebrates progress and is supportive. Additionally, features like early paycheck access may undermine budgeting goals by encouraging earlier and potentially increased spending, conflicting with the app’s core mission of financial discipline.

Elijah

EveryDollar

Website

Description

EveryDollar is a budgeting app built around the zero based budgeting method, where users assign every dollar of monthly income to a specific category before the month begins. It is associated with Ramsey Solutions and is designed for people who want a structured, rules-driven approach to money management, especially users who are trying to control spending, get out of debt, or stop living paycheck to paycheck. The product experience centers on planning rather than simply tracking, with categories for fixed expenses, variable spending, savings, and debt payments. Its core market need is reducing financial overwhelm by giving users a simple system that turns “I do not know where my money goes” into an explicit plan for how money will be used.

Strengths and Weaknesses

A major strength of EveryDollar is that it is easy to understand and operationalizes a clear budgeting philosophy. The zero based format makes the user set priorities up front, which can be motivating for people who want structure and a sense of control. The category layout is straightforward, and the interface is typically uncluttered, which lowers the barrier for beginners who are new to budgeting. It also supports routine budgeting behaviors like planning monthly categories, reviewing remaining amounts, and making adjustments as spending occurs, which reinforces consistency over time. The app’s weaknesses mostly come from rigidity and feature tradeoffs. The strict budgeting approach can feel inflexible for users with irregular income, fluctuating bills, or unpredictable schedules, because it assumes the user can confidently plan a month in advance and keep categories stable. In addition, bank syncing is not always available without a paid plan, which increases friction for users who want automatic tracking rather than manual entry. Finally, EveryDollar is strong on “what you planned” but weaker on “why you spent,” meaning it does not deeply support reflection on context, emotions, or triggers that influence spending, which can limit behavior change for users who struggle with impulsive or stress-based purchases.

Upside

Website

Description

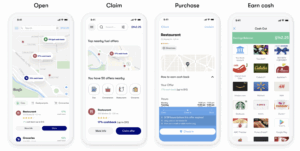

Upside is a cash back rewards app that helps users earn money back on everyday purchases, most commonly gas, groceries, and restaurant spending. It targets cost conscious users who want immediate savings without doing complex budgeting or changing their routine dramatically. The experience is offer based and location based: users find nearby deals, make a purchase at a participating business, and then claim cash back through the app. Upside’s unique role in the market is that it makes saving feel rewarding and effortless by tying benefits directly to purchases that users already make, which appeals to people who want quick wins and simple value rather than long-term planning tools.

Strengths and Weaknesses

Upside’s biggest strength is that it provides a clear and tangible benefit with low effort. The value proposition is easy to explain, earn cash back on purchases you were already going to make, which helps with adoption and repeat use. The interface is typically designed around convenience, showing nearby offers, estimated earnings, and simple steps to claim rewards, which reduces friction and makes the app feel immediately useful. It also creates a positive feedback loop: seeing rewards accumulate can motivate continued engagement, especially for frequent drivers or users who regularly buy gas or eat out. The weaknesses are that it is transaction and incentive focused rather than behavior and goal focused. Because the app rewards spending, it can unintentionally encourage users to purchase more often or choose a merchant because of cash back rather than because it aligns with their financial goals. It also does not help users see their full financial picture, track budgets across categories, or understand patterns behind their spending decisions. The app’s usefulness depends on partner coverage and location availability, so the experience can vary a lot based on where the user lives and what merchants participate. Finally, Upside supports short-term savings but does not address deeper needs like habit building, planning, or reflection, so it may not help users who want lasting changes in how they manage money.

Cyan

Acorns

Website

Description

Acorns is an investing application that rounds up daily purchases to the nearest dollar and invests them into a portfolio of Exchange-Traded Funds (ETFs). Their application brings together checking, savings, investing, and retirement all in one place. They target a range of individuals at various stages of their financial journey, including people who are beginners at investing, people trying to save money for their kids, people who are planning for retirement. Their website claims “Wherever you are on your money journey, Acorns’ financial wellness tools can help you reach your goals.” Their core features included their automated investment and banking (i.e., checking and savings) .One of the key markets that the Acorns application fulfills is lowering the barrier to entry for investment.

Strengths and weaknesses

Acorns is described as a beginner friendly way to invest based on its automated investing features. On reddit, one user wrote .“Honestly, I never noticed the money leaving my account. Round-Ups make it easy to invest without thinking about it.” The simplicity of the application is also noteworthy, given that it is an all-in-one financial solution. People can invest, bank, and retire all in one place. There is also no minimum to open an account. On the flip side, flat fees can be high for users with small balances. A reddit user wrote, “I was paying $3 a month, but my balance was only around $400. That’s more than 9% annually just in fees. Moved to another platform.” Moreover, portfolio options are limited and users have no access to human financial advisors. A key gap in Acorns that our application will aim to address is reducing friction for users with lower balances, thereby improving the experience for those early in their financial savings journey.

Rakuten

Website

Description

Rakuten is a free cash-back shopping platform. Users can earn cash-back from more than 3,500 stores through using Rakuten’s application, browser extension, or website. Their target audience include digitally engaged consumers and savvy shoppers. Some of Rakuten’s unique features include the ability to stack rewards, real cash back via Paypal or a check (instead of points or a gift card), and AI-driven personalized shopping recommendations. Rakuten fulfills a market need for savings for everyday consumers, by helping people save money through cash-back and rewards. They are also an alternative to using Amazon.

Strengths and weaknesses

Some strengths of Rakuten include the ease of receiving cashback, that it is free to use, and that it works with a large variety of retailers. A major weakness, however, is the collection and selling of user data. One user on Reddit wrote, “Just make sure you think the loss of privacy is worth the saving for you.” Unlike Rakuten, our application will value user privacy. We will aim to present a solution that saves users money without selling their data. Rakuten also assumes that people already have the money to spend at retail stores, whereas our application can offer support for low-income users.

Bennie

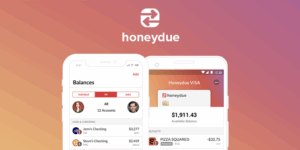

HoneyDue

Website

Description

Honeydue is a free, mobile-only budgeting app designed specifically for couples to manage shared finances transparently. The app targets romantic partners at all relationship stages who want to coordinate spending, track joint expenses, and improve financial communication without merging all of their accounts. Honeydue fulfills the market need for relationship-specific financial tools that balance transparency with individual privacy; users can link both joint and individual accounts, set customizable privacy controls for each account (showing full transactions, balances only, or hiding accounts entirely), create shared budget categories with spending limits, receive bill reminders, and communicate through an in-app chat feature with emoji reactions on specific transactions.

Strengths and weaknesses

Honeydue has many strengths that show a genuine interest in uplifting serviced couples; it is completely free with no features locked behind paywalls. The flexible privacy controls let couples maintain financial independence while collaborating on shared expenses (reflects the interactions on which the platform is based). The in-app chat and emoji features reduce friction around money conversations by keeping financial discussions in context rather than requiring separate apps or face-to-face conversations. However, some weaknesses include being mobile-only with no desktop access, limiting usability for users who prefer larger screens or computer-based financial management. The platform also lacks advanced features like investment tracking, detailed financial reports, or long-term planning tools. Also, some users report occasional account syncing delays, and recent updates removed features like Support Chat and the Tip Jar (declining customer support responsiveness suggesting potential product maintenance issues).

Penny Finance

Website

https://www.penny-finance.com/

Description

Penny Finance is an online financial planning and education platform designed primarily for women who lack access to traditional financial advisors. Founded by Wall Street veteran Crissi Cole, the platform targets women aged 18-75, particularly those dealing with student loans, debt, and retirement uncertainty. Penny Finance addresses the market gap where 7 in 10 women don’t have financial mentorship, providing personalized financial plans, educational masterclasses, investment guidance, and a moderated community forum. The platform connects users’ financial accounts through Plaid integration to provide real-time insights and custom recommendations for debt payoff strategies, savings goals, and retirement planning.

Strengths and weaknesses

Some strengths of Penny Finance include their highly personalized approach with tailored financial plans that adapt to individual circumstances and life stages, a strong educational component with masterclasses, workshops, and digestible content that demystifies complex financial concepts, and a community feature that provides peer support and reduces isolation around money topics. Some weaknesses include being focused primarily on planning and education rather than day-to-day spending behavior modification and requiring a paid membership subscription. Those more interested in adjusting their spending rather than reframing saving may not enjoy how the platform emphasizes long-term financial wellness over immediate spending control. As far as the mission can go, the women-first branding may limit appeal to broader audiences. Finally, the nature of the product being saving-based means that the product itself lacks features for real-time purchase decision-making or preventative spending controls.

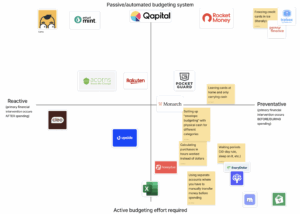

2×2 Map

Reasoning

This 2×2 map organizes financial tools along two dimensions that are especially relevant to impulse and convenience-based spending: timing of financial intervention (reactive vs. preventative) and level of budgeting effort required (passive/automated vs. active). These axes matter because behavior change depends not only on awareness, but on when an intervention occurs and how much effort it demands from users. Our research and diary studies suggest that interventions after spending often raise awareness but rarely prevent repeat behavior, while highly effortful systems are effective but difficult to sustain.

Tools, such as Intuit Mint and Earny, are placed in the passive, reactive quadrant because they largely intervene after spending has occurred. Mint automatically aggregates and categorizes transactions to show where money went, while Earny tracks prices and refunds users when prices drop. Cleo also sits on the reactive side, since its insights and “roasts” typically occur after purchases. We placed it as more active because users must engage directly by chatting with the bot, responding to prompts, and participating in mini games.

On the active end of the spectrum, tools like Excel spreadsheets, YNAB, and EveryDollar require users to manually plan, categorize, and reflect on spending. These systems are more preventative because they encourage intentional allocation before spending, but they demand sustained effort and discipline. Physical and behavioral strategies, such as freezing credit cards, waiting periods, or cash envelope systems, are placed in the preventative quadrants because they introduce friction directly at the point of purchase, even though they require high user effort.

Finally, tools like PocketGuard and Monarch Money sit closer to the center, blending automation with light planning. PocketGuard simplifies decision-making by showing a single “safe to spend” number, while Monarch combines automated tracking with optional goal-setting or rules. Overall, the map highlights a crowded space around preventative tools and automated tools.