Team 4: Tara Jones, Devorah Simon, Raagavi Ragothaman, Chloe Liu

This image was created with the assistance of DALL·E 2

Problem Statement

The problem space that our team chose to focus on was the issue of financial awareness among young adults. We knew anecdotally that college students struggle with learning to budget and how to properly manage their finances. Since many budgeting apps are designed for more well-established adults, with stable rates of inflow and outflow, we wanted to direct our attention towards providing a more holistic approach to finances.

Baseline Study

We screened for participants in the 18-25 age range. In our pre-study interviews, we asked about tools that young adults use for budgeting/financial tracking. We also wanted to test our hypothesis that financially independent participants would be generally better-aware of their financial state. We also asked for some context about their own concerns related to their spending. Finally, we asked them if they could divide their approximate spending into percentages. We used this to judge a participant’s financial awareness based on how accurate their pre-study prediction was. The interview script/responses can be found here.

For the baseline study, we asked participants to record their actual spending for each day as well as what they anticipated spending the next day, divided by category. We then followed up with a post-study interview that mimicked the structure of the pre-study interviews, to understand changes. We also asked if there was anything about their spending habits that had surprised them, to see if there were any patterns that they had noticed individually.

We then mapped our findings according to several configurations, including affinity mapping and story mapping here. Several key insights then guided our eventual intervention study design, including the existence of multiple factors influencing awareness as well as the significant, outsized role that emotional spending plays in the finances of young adults.

Comparative Research / Analysis

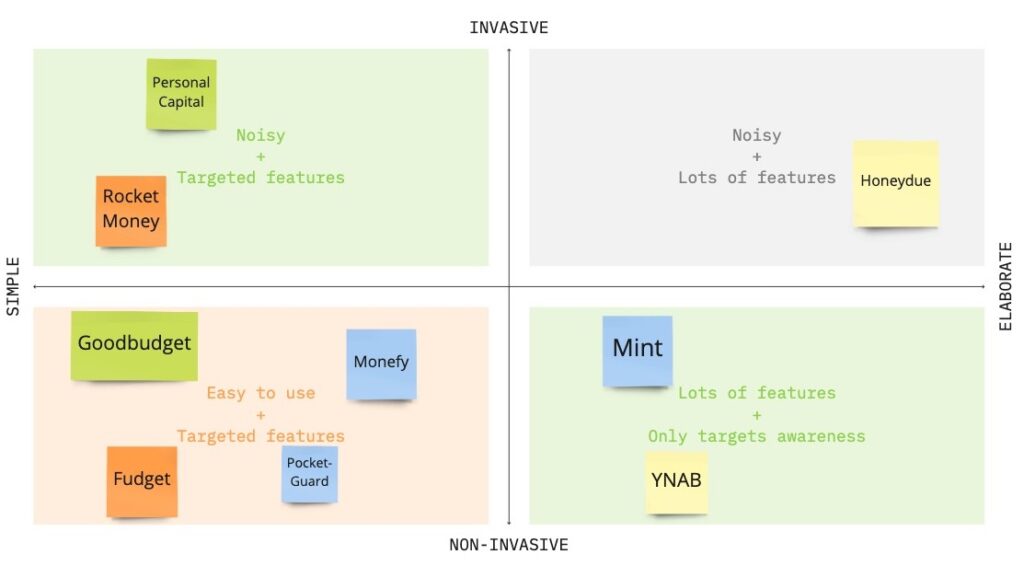

We did a comparative analysis of 8 personal finance apps to explore the existing solutions and look for new opportunities. Some of them were featured by comprehensive functionalities. For example, Mint is a personal finance app launched by Intuit that allows users to manage all aspects of their financial life in one place. Some others target different user groups. For example, Personal Capital has financial advisors that can help users create a retirement plan; Honeydue is designed as a financial tracker for partners. Although their users are different from ours, we learned the benefit of narrowing down the target audience. A major weakness we identified in these existing apps was the lack of incentive. They mostly just provide functionalities to organize personal finance, but once the users become less motivated they barely have any way to bring them back to the app, leading to a low retention rate. We decided to combat this weakness in our design.

We came up with a 2×2 mapping simplicity vs invasiveness. Mint, for example, is on the elaborate side. If an app aims to change the users’ behavior by providing intrusive reminders or suggestions, it is on the invasive side. One key insight we draw from the 2×2 is the simpler the better. Most successful personal finance apps have a clear UX design and targeted features.

We hope to distinguish our app from the existing solutions by targeting young adults, providing concise features and adopting a sustainable reward mechanism.

Literature Review

We have also done a literature review to equip ourselves with more theoretical knowledge. This study indicates that a change in budgeting intention requires acquiring more financial knowledge and changing attitudes toward money management. However, some other studies indicate that financial education itself is not sufficient in shaping financial behaviors. This article argues that although traditionally behavior change has been viewed as a result of changes in people’s beliefs, attitudes, etc, we can also change behavior by subtle changes to the environment within which decisions are made. Similarly, according to this and this paper, the assumption that improved knowledge will result in more effective financial decision-making is sometimes wrong since factors such as income, financial satisfaction, financial confidence and education also matter. We also learned from this paper that recording personal spending helped spenders maintain their spending levels and better meet their own expectations.

After diving deep into these research and studies, we confirmed that an online personal finance app is the solution we will stick to, and through our app, we will help increase incentives to organize personal finances, and design features that can naturally fit in users’ daily routines to seamlessly change behavior.

Personas and Journey Maps

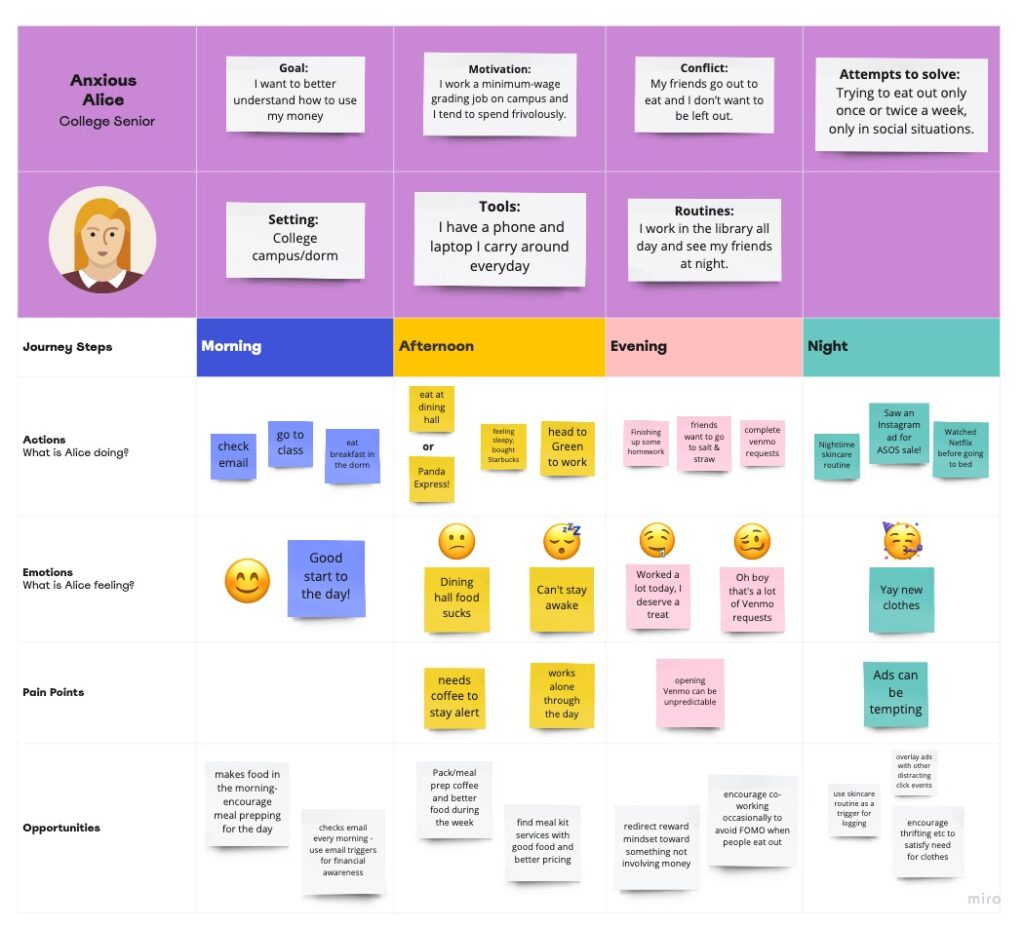

From our baseline studies, we were able to further divide the target demographic into 2 broad categories. The first category was college students that were not entirely financially independent but were earning enough to support their discretionary spending. Pain points within this demographic often include the need to spend money on food and a general unawareness of spending until credit card bills need to be paid as well as feelings of anxiety and heightened emotions surrounding money. Anxious Alice below captures the traits of users we observed in this group.

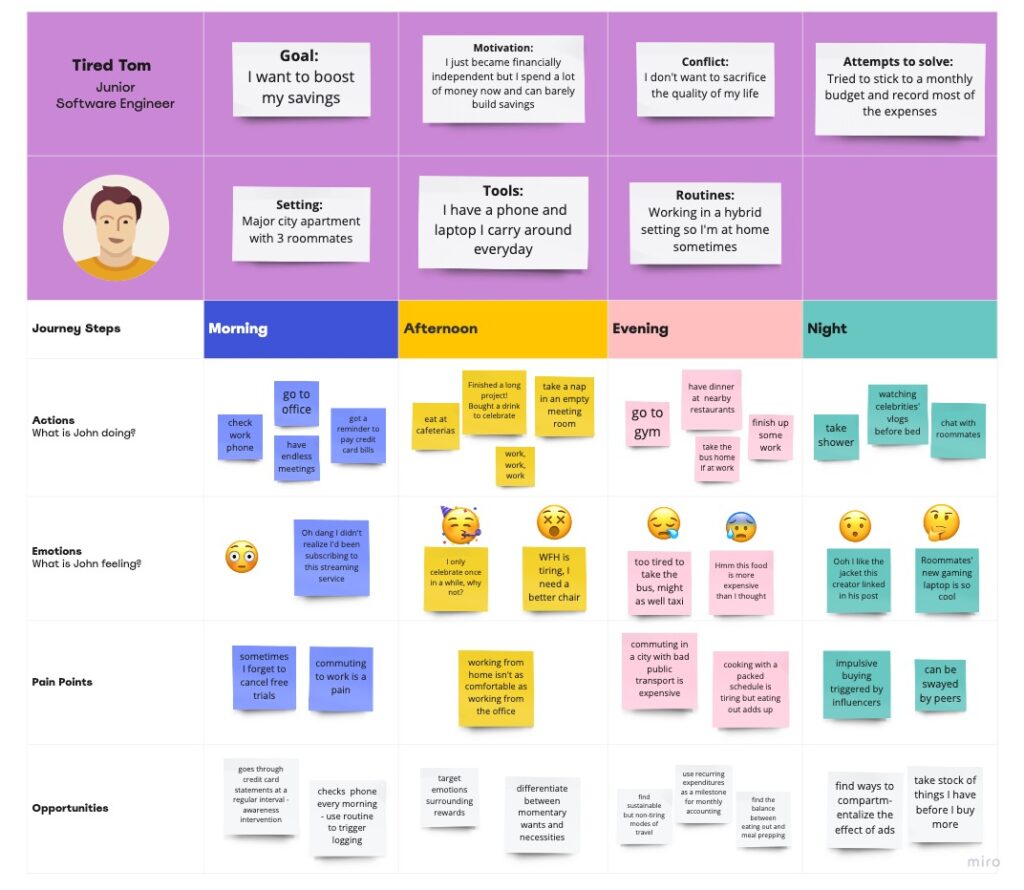

The second category was recent college grads who have recently started earning full-time salaries or are trying to navigate the professional world in some way. Pain points in this demographic were everyday issues such as commuting and impulsiveness influenced by financial independence. Tired Tom’s life gives us a glimpse of major spending triggers for people in this group:

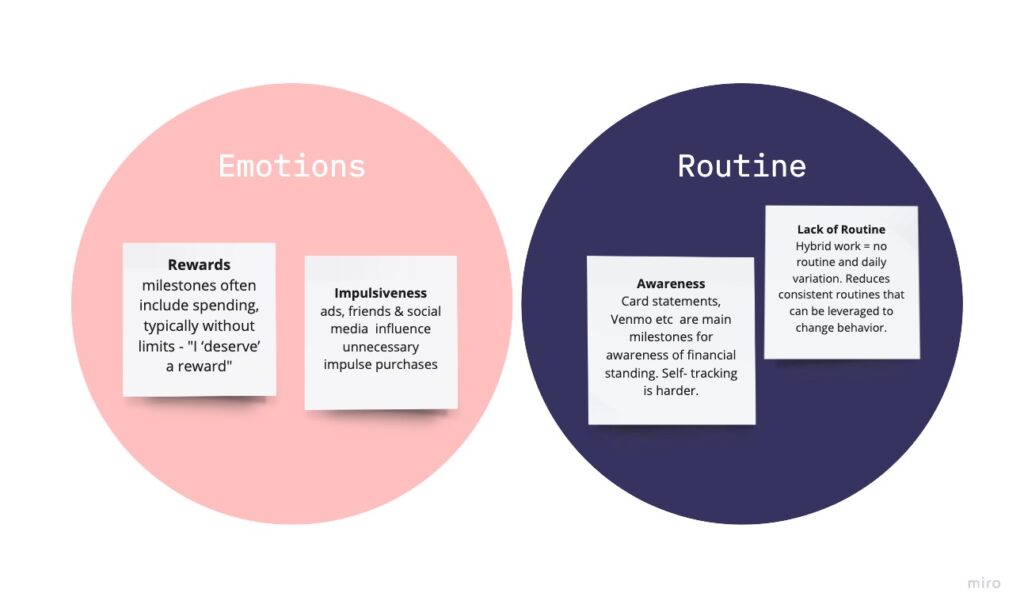

There were several insights we gained from these journey maps, specifically with regards to routines, pain points and opportunities. We identified two broader themes that these insights fit into and tried to model our intervention ideas with these themes in mind. Some novel insights included:

See an in-depth analysis of our personas here.

Intervention/Product Ideation

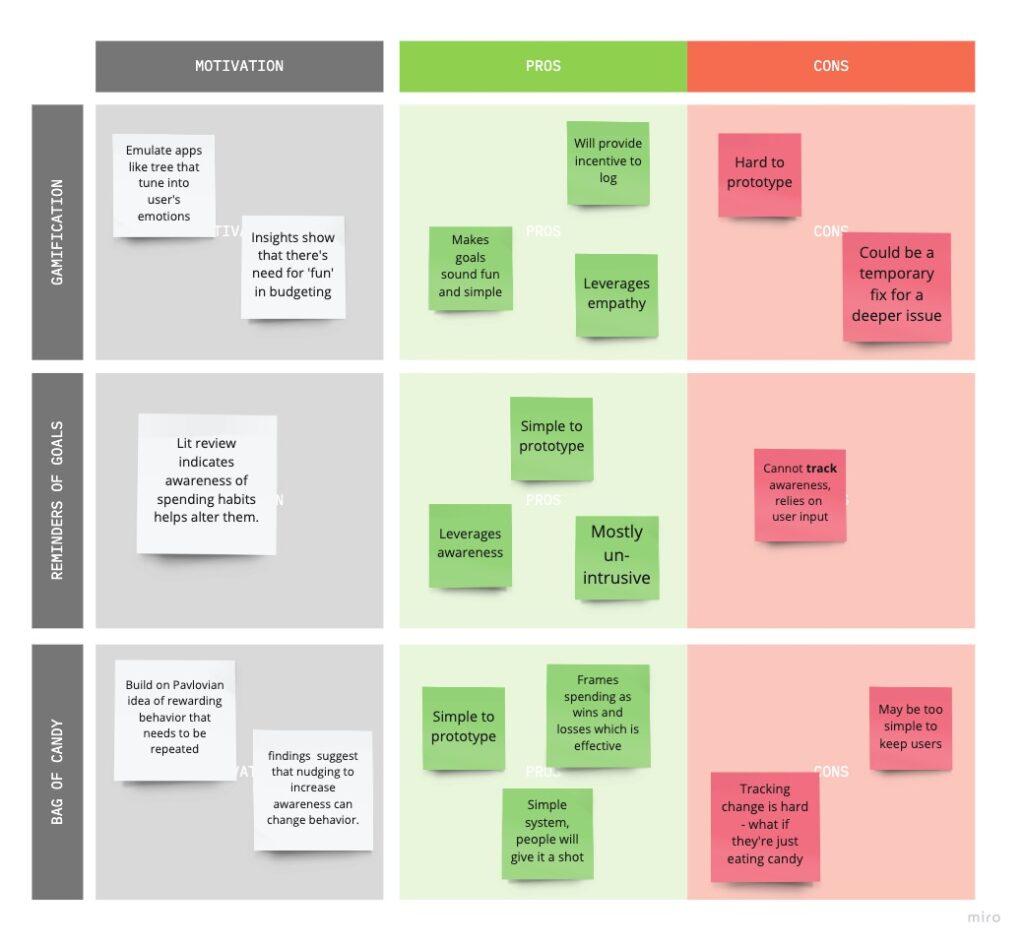

We tried to target two primary pain points that we learned of from the baseline study and journey maps: 1) making budgeting and financial tracking more fun, reducing negative emotions associated with it while still increasing awareness and 2) keeping the system simple and accessible without overloading the user with numbers. Some of the ideas we deliberated include:

- Gamified Budgeting: Use participant reports of their daily financial habits and goals that we have them set the previous day to simulate a simple game and construct their progress on the game as a product of their financial habits. We ask for their progress at 12 hour intervals and send them a message with their position in the game.

- Simple, moderately intrusive reminders of personal goals: Send the participant reminders at infrequent intervals of their budgets for specific categories for the day and then records how those goals were met at the end of the day.

- Buy yourself a bag of candy, everytime you make a purchase, log it, and then eat a candy: Each participant has a bag of candy from which they eat a candy each time they spend money and remember to log the expenditure.

See an in-depth comparison of our ideas here.

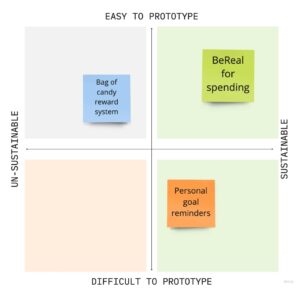

To narrow down the system we wanted to test, we took into consideration our own capabilities as developers of this system and the users’ experiences as long term users of the system. We mapped the ideated systems on the 2×2 above according to ease of prototyping and whether or not the system was sustainable long-term.

Thinking about gamification and its issues with sustainability, we were able to rethink that system to more closely resemble BeReal – as a platform that is fun and encourages accountability but is not majorly intrusive or overwhelming. Based on this, we were able to identify ‘BeReal for budgeting’ as a sustainable, easy to prototype system tackles both the major pain points we were attempting to mitigate. BeReal since its inception has achieved a surprisingly sustainable way of making people perform a certain action once a day and we’re seeking to emulate that behavior without bothering the user at regular intervals.

Intervention Study

Goal: Help users gain more understanding of their daily spending habits through a small task- a selfie every time they make a process.

Hypothesis: Taking a selfie every time one buys something will make the users more aware of their financial habits, and force them to reflect on their emotions related to certain purchases.

Methodology: 5-6 participants, contacted through text message. Users send their contact in the study a selfie every time they make a purchase.

Target audience: 18-25 year olds

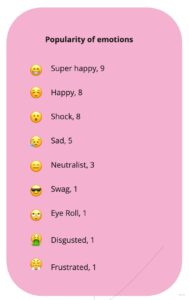

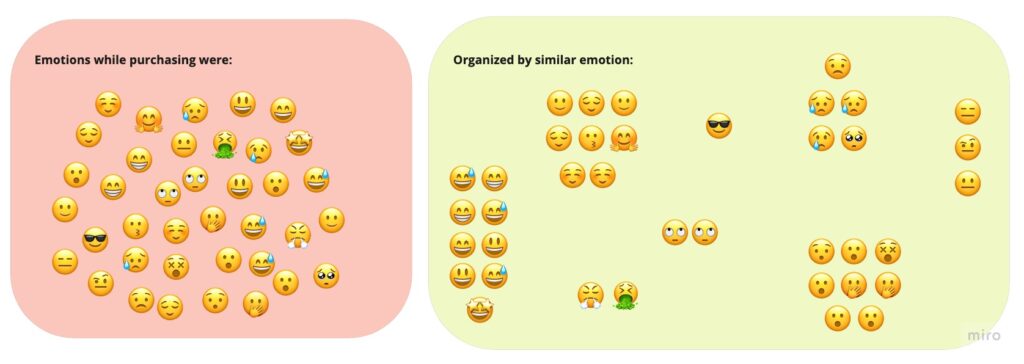

Synthesis: The participants in the study reported that taking pictures of their spending did not significantly change their spending habits. However, the process did remind them of their previous spending and made them more aware of how many times they spent money in a day. In one instance, it made them reconsider buying a dessert at dinner, but they were already unsure about spending $10 on it. The participant was surprised at the number of times they spent money when they sent the emojis at the end of the day. They typically knew how much they spent in a day, but not how many times. The participants spent money on various meals, including breakfast, lunch, and dinner, as well as at the airport. Overall, the study may not have changed their spending habits, but it did make the participant more grateful for having money to spend and for the things they spent it on, which they considered worth it.

There are a few takeaways from this study that we can use to improve spending habits. Firstly, the study reminds us of the importance of awareness. Even if we have a rough idea of how much we’re spending, we may not be aware of how many times we spend money in a day or week. Taking pictures and using emojis to track spending can help us become more aware of our spending habits and help us make better financial decisions.

Additionally, the study highlights the value of emotionally budgeting. While it’s important to have a budget and track our spending, we can also benefit from taking a more flexible approach that allows for unexpected expenses. By adjusting our spending based on informed intuition, users can make better financial decisions and avoid overspending.

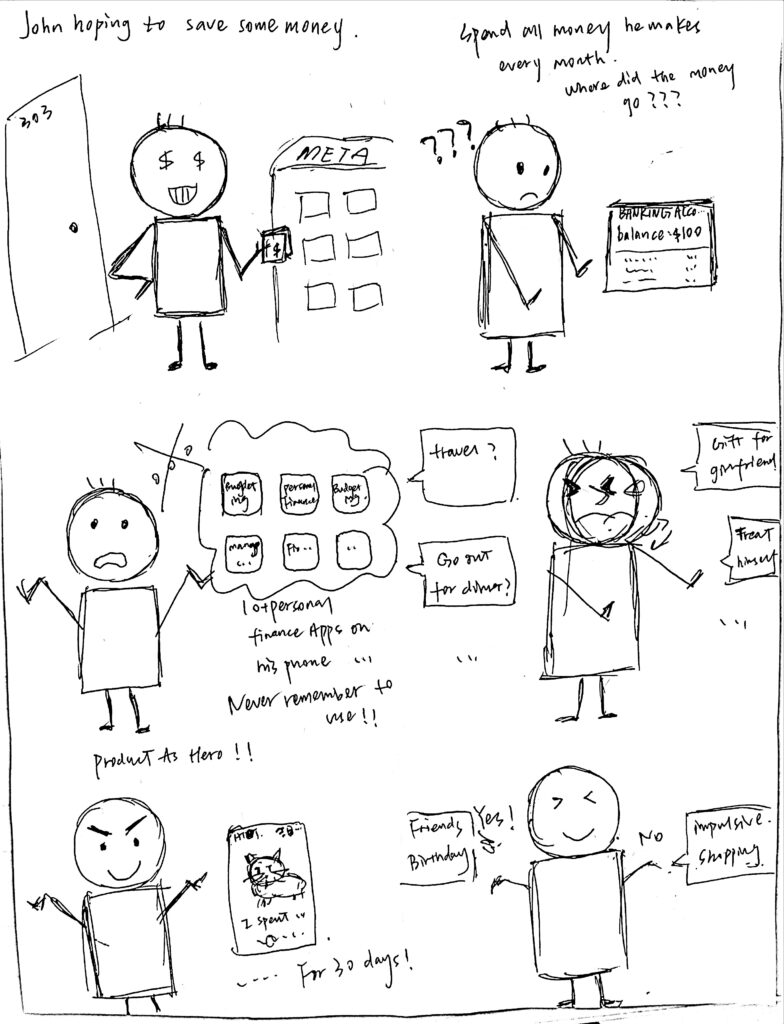

Storyboard & Stories

Our storyboards describe two types of people that might benefit from easier financial planning. Tired Tom is frustrated with budgeting apps and decides to spend intuitively. However, this intuition revolves around the comfort of a single paycheck and will likely cause bills to add up in the long-run. John on the other hand attempts to use a financial tracking app but frequently forgets to log his spending and runs into similar problems to Tom.

Key Insights: We learned that spending is often a low effort alternative to activities like cooking that take time and energy. This low barrier to usage makes money easy to spend and difficult to track, regardless of one’s goals. This insight also informs what kinds of apps people are likely to use sustainably. We hope to provide a solution which employs the lowest possible effort while capitalizing on the possible recurrence of expenditure to provide users with better lazy visibility of their spending.

Current Direction

As we continue on with this project, we will be using the insights from prior parts to form our application prototype. We will be using gamification in order to motivate users to make smart financial decisions, and to encourage them to stick with “the program.” From the success of the intervention study, we are going to employ a similar “BeReal,” but putting in more reminders/structure to this process. One aspect that our team needs to consider moving forward is the feasibility of testing gamification on a Figma prototype. We want users to feel the experience of having incremental wins with their financial literacy.

Questions

- Are there any ethical implications of using this method of gamification and making budgeting ‘fun’?

- How do we ensure that this is a sustainable way of addressing the root cause of excess spending and not a band-aid solution?